Chargebacks: Demystified for Indian Businesses

For Indian Enterprise Businesses, whether publicly listed companies or scaling startups — chargebacks are more than just a minor inconvenience. Poor chargeback management can inflate costs, damage brand reputation, and disrupt revenue streams.

This blog demystifies the complex world of chargebacks, offering enterprises actionable insights to tackle them head-on and turn them into opportunities for growth and improvement.

What is a Chargeback & Why do they happen?

A chargeback is like a ‘financial boomerang’. It’s when someone disputes a charge on their credit or debit card with their bank, saying, “Hey, this wasn’t right!”. Instead of reaching out to you for a refund, they go straight to their bank, dragging you into a process you didn’t even sign up for.

Now, why does this happen? :

Fraudulent transactions: Someone uses a stolen card to make a purchase, and the rightful cardholder disputes the charge.

Not-so-satisfied Customer: They didn’t get what they ordered, weren’t happy with what they got, or just had a change of heart — and instead of calling you, they called their bank.

Processing Errors: Mistakes like billing the wrong amount or charging someone twice.

Unrecognised Transactions: The customer doesn’t recognise your business name on their statement, and they think, “This isn’t me!” Boom, chargeback filed.

While some of these are valid, in a few cases the customer raises a dispute just because they can!

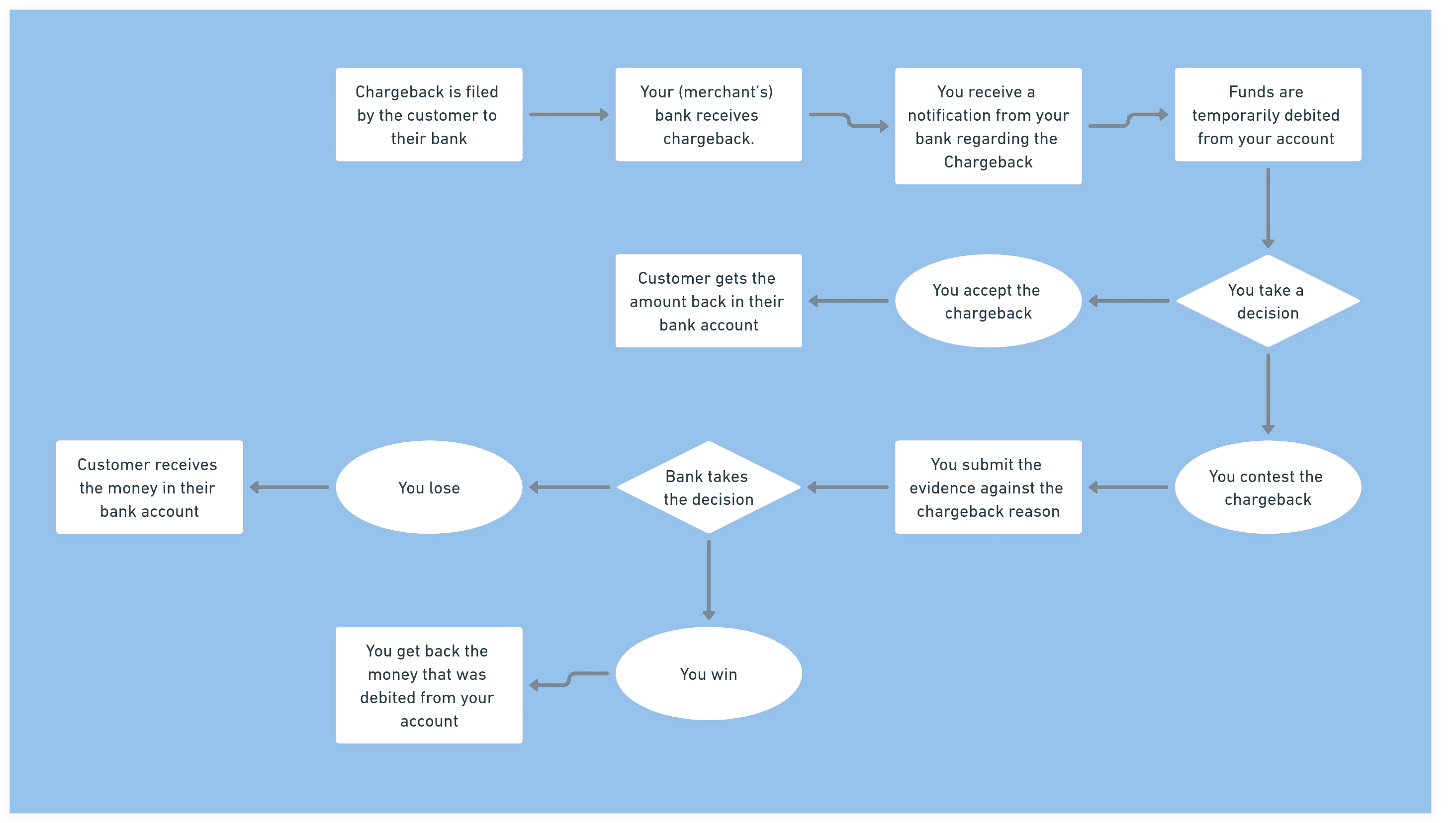

Chargeback Lifecycle: From Initiation to Resolution

Here’s the typical lifecycle of a chargeback:

Initiation: A customer disputes a charge with their bank, claiming fraud, dissatisfaction, or an error. The bank starts investigating.

Review: The card issuer reviews the claim and decides if it’s valid. If yes, the chargeback is officially filed, and the money is pulled from your account.

Notification: You, the merchant, get notified about the chargeback and are asked to respond.

Response: If you disagree with the chargeback, you submit evidence (like receipts, delivery confirmations, or customer communication) to challenge it.

Resolution: The bank reviews the evidence and makes a decision. If you win, the money is returned. If not, the chargeback stands.

Timelines and Costs when you’re facing a Chargeback

The chargeback process is tightly regulated, with timelines ranging from 30 to 120 days depending on the dispute type and payment method. Acting quickly is crucial because missing deadlines often means losing the dispute automatically.

Costs? They can add up fast! Each chargeback costs around Rs 1500 in fees, not to mention the lost revenue and operational costs of fighting disputes. High chargeback ratios could also lead to penalties or even termination of your merchant account by payment processors.

Staying proactive with monitoring and evidence submission can save you both time and money in the long run!

Strategies to Prevent & Reduce Chargebacks

The best strategy is to stop disputes before they even start. Here’s how to protect your business and keep your customers happy:

Nail the Basics: Operational Best Practices

Use plain language in invoices, receipts, and terms of service. Let customers know what to expect.

Educate and Empower Your Customers

Send Proactive Emails: If something goes wrong — like a delayed delivery — email customers with refund options and include your billing descriptor for clarity.

Accessible Refund Options: Make it easy for customers to request refunds directly on your website or portal. If they feel heard, they’re less likely to go straight to their bank.

Use Technology to Your Advantage

Turn On 3D Secure (3DS): This extra authentication step can prevent fraud-related chargebacks.

Fraud Prevention Tools: Use tools like tokenization, address verification (AVS), and CVV matching to catch suspicious transactions.

Stay Close to Your Customers

Store Contact Information: Keep customer phone numbers handy. If a chargeback is filed, reach out and politely request them to withdraw the dispute if you’ve resolved the issue.

Exceptional Support: Be easy to reach via chat, email, or phone. Happy customers rarely file chargebacks.

Build Internal Safeguards

Monitor Transactions: Set alerts for high-risk transactions or unusual purchase patterns.

Keep Records: Store receipts, delivery confirmations, and customer communication to use as evidence if needed.

What to do when you receive a Chargeback?

When a chargeback lands in your inbox, it’s go-time. Here’s how to handle it effectively, with specifics to boost your chances of winning the dispute:

Review the Chargeback Reason Code

Each chargeback comes with a reason code provided by your payment processor. This code tells you why the chargeback was filed — fraud, non-delivery, defective goods, or something else. Understanding this is key to crafting a relevant and strong response. You can check out the popular reason codes here.

Gather the Right Documentation

To challenge a chargeback, you’ll need to present clear, compelling evidence. The type of documentation you’ll need depends on the situation:

Delivery Issues: Proof of delivery, tracking numbers, or signed confirmations.

Unauthorized Transactions: Customer authorization (AVS/3DS), IP/geolocation data, or access logs.

Cross-Border Sales: Customs clearance and delivery confirmation.

Damaged Goods: Photos of the product’s condition and return/warranty policies.

Respond Within the Deadline

Chargeback disputes have strict timelines, often as short as 7–10 days. Miss this window, and you forfeit your chance to fight the chargeback.

Be Concise and Professional

Stick to facts, keep it concise, and back your response with solid evidence for the best chance of success. Use a checklist format for your evidence to make it easy for the bank to review.

Conclusion: Your Payment Processor — The Key to Chargeback Control

Managing chargebacks doesn’t have to be a battle you fight alone. With clear customer communication, proactive fraud prevention, and streamlined dispute resolution, you can significantly reduce the risk of chargebacks. But the real game-changer? A payment processor that has your back.

At xPay, we provide the tools and support you need to stay ahead of chargebacks. With features like 3DS, real-time fraud detection, and hands-on assistance, we ensure your transactions are secure and your disputes are manageable.

Choose a payment processor that helps you focus on growth, not chargebacks. Try xPay here!